Pension reform strengthens pension financing

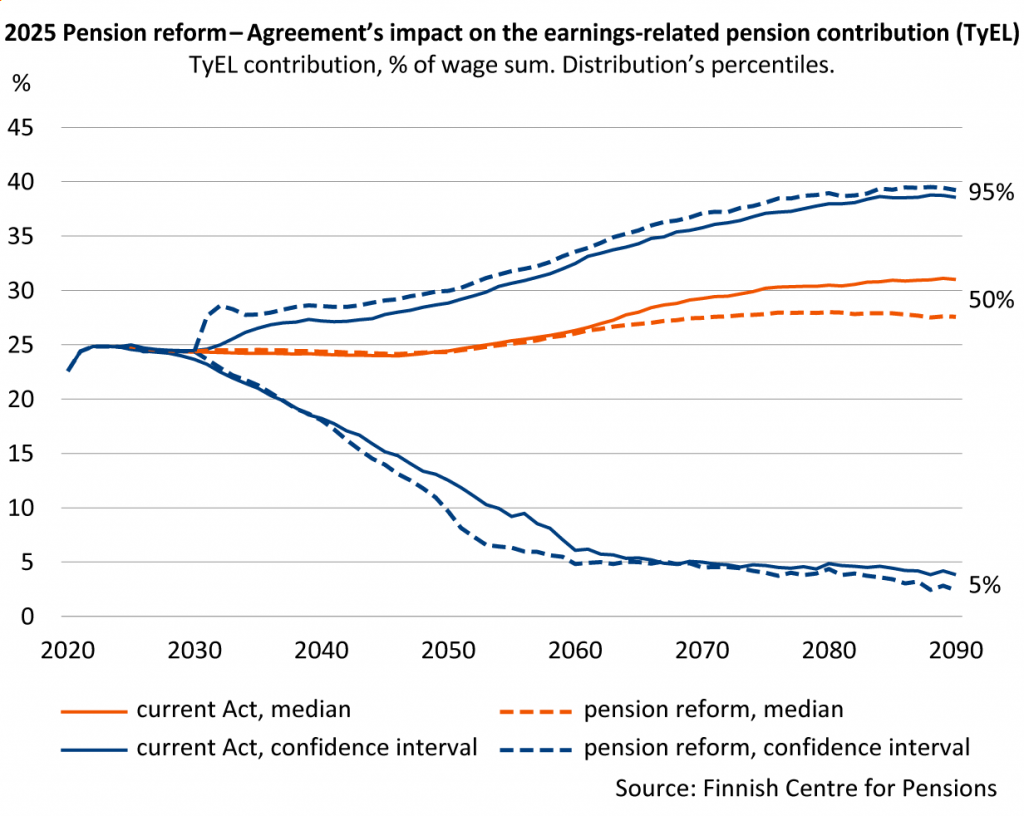

According to the calculations of the Finnish Centre for Pensions, the reform strengthens pension financing. Estimated at the contribution level, the overall reform would reduce the pension contributions under the Employees Pensions Act (TyEL) by, on average, 1.5 percentage points. The equity weight will rise which will increase the pension assets. Pensions will be determined as before, and there will be no change to age limits up to 2030.

One of the objectives in the Government Programme is that the pension reform must secure the financial sustainability of the earnings-related pension system and adequate pension levels. The reform must strengthen public finances in the long run by around one billion euros.

According to the outcome of the negotiations between the labour market organisations concluded on 19 January 2025, the objective will be achieved through a moderate investment reform and other measures.

The Finnish Centre for Pensions assesses that the most significant components of the reform are the changing regulations that support increasing investment returns, additional funding of old-age pensions and the inflation stabiliser.

According to estimates of the Finnish Centre for Pensions, following the reform, the proportion of shares in the investment portfolios could increase by more than 10 percentage points , while the weight of other investments would decrease. Following these changes, the expected real return for private sector pension assets could improve by around 0.3 percentage points compared to current regulations.

The earnings-related pension contribution under TyEL will be stabilised at 24.4 per cent up to 2030. The share of funded old-age pensions will increase. The inflation stabiliser mitigates the index increases in earnings-related pensions in exceptional situations where consumer prices would develop faster than wages over the two-year review period.

According to the calculations of the Finnish Centre for Pensions, the reform strengthens pension financing in the long term. The overall reform would reduce the TyEL contribution by, on average, 1.5 percentage points. Around one fifth of this improvement will be due to the change in the funding of old-age pensions and one fourth to the introduction of the inflation stabiliser.

The age limits and how pension benefits are determined will not change, making this reform different in nature from other pension reforms of the 21st century.

“The reform responds to the pressure to increase pension contributions caused by decreasing nativity by increasing the role of pension assets and funding. The share of the changes in investment operations and funding accounts for around 70 per cent of the total impact of the reform”, says Mikko Kautto, Managing Director of the Finnish Centre for Pensions.

Reform increases pension investment return fluctuations

The investment activities of private sector pension providers are governed by solvency regulations, which aim to ensure the payment of pensions and the continuity of insurance activities.

The reform amends the regulations so that earnings-related pension providers can take higher risks when investing pension assets to improve investment returns. Regulatory changes aim to increase the equity weight of investments and avoid forced sales in bad times.

Increasing the investment risk increases return fluctuation: in good times, the returns may be more favourable, in bad times weaker than currently.

“There’s another side to the coin, too. If investments yield poor returns for a long time, earnings-related pension contributions might need to be increased more than under current legislation as a result of the reform”, says Heikki Tikanmäki, Development Manager from the Finnish Centre for Pensions.

Inflation stabiliser adjusts earnings-related pension index

The pension reform introduces a new partial stabiliser. The stabliser affecting the entire earnings-related pension system curbs the growth of the earnings-related pension index which raises earnings-related pensions annually, if the index increases faster than the wage coefficient over a two-year period. The inflation stabiliser is expected to be in operation by 2030 at the earliest.

Situations in which a stabiliser would reduce the earnings-related pension index have been very rare.

“In the light of history, it is rare for prices to rise faster than earnings two years in a row. That is why the significance of the inflation stabiliser is estimated to be small compared to, for example, the life expectancy coefficient”, explains Kautto.

If the inflation stabiliser had been in operation under the high inflation conditions between 2022 and 2023, the total effect of the adjustment of an average earnings-related old-age pension of 2,000 euros would have been around 70 euros lower than the realised one. In 2024, the effect would have been around four percentage points lower than under current regulations.

2025 Pension reform – objectives and key actions

- the objective is to secure the financial sustainability of the pension system and adequate pension levels;

- the changes must strengthen public finances in the long run by around 0.4 percentage points relative to GDP, or about one billion euros;

- the reform aims to increase the investment returns on pension assets by changing the investment regulations that apply to private sector earnings-related pension providers;

- includes an agreement on a contribution rate of 24.4% for private sector earnings-related pensions (TyEL) for the period from 2026 to 2030;

- includes an inflation stabiliser that curbs index adjustments to earnings-related pensions if the earnings-related pension index increases faster than the wage coefficient over a two-year period;

- does not change current pension benefits, such as the retirement age and pension accrual rates.

Investment reform

- is part of the pension reform and improves the opportunities for private pension providers to pursue better returns on pension assets;

- raises the equity-linked buffer fund to 30% which, in turn, allows for an increase of the equity weight of investments to a maximum of 85%;

- lowers the solvency limit to 95%, which reduces forced sales of investments at unfavourable times;

- expands access to leverage in real estate investments and limits premium lending;

- increases the investment risks and return fluctuation of pension assets for better or worse;

- does not change the basic principle stated in law that pension assets must be invested profitably and securely.

Inflation stabiliser

- is a new mechanism affecting the index adjustments of earnings-related pensions are determined;

- curbs the annual index increases of earnings-related pensions if consumer prices rise faster than wages over a two-year period;

- is technically linked to the development of the earnings-related pension index and the wage coefficient;

- will enter into force after 2030 at the earliest;

- can be considered an automatic stabiliser. The first automatic stabiliser was introduced in the Finnish pension system in connection with the 2005 pension reform. At that time, the pension-adjusting life expectancy coefficient was agreed on. In connection with the 2017 pension reform, the retirement age for the old-age pension was linked to life expectancy.

More information:

- Finnish Centre for Pensions, Media Services, phone +358 29 411 2920 (weekdays 9:00 a.m.- 4:00 p.m. EET)

Read more