International investment performance of pension funds: Finnish funds securing top positions

The investment year 2024 was surprisingly good for pension funds worldwide. In the international performance comparison conducted by the Finnish Centre for Pensions, the average real return exceeded long-term figures. Finnish pension funds were among the best in their category.

According to the Finnish Centre for Pensions’ annual investment comparison, 24 pension investors from nine different countries achieved an average nominal return of 9.5 per cent after expenses last year. The average real return was 8 per cent.

“Despite the recent trade wars that have shaken global stock markets, many pension investors have actually had an exceptionally good investment year. Last year’s return was well above long-term figures,” says Liaison Manager Mika Vidlund.

The impact of inflation on pension investors’ real returns is significant.

“Although inflation has fallen in many countries, it has affected the results of the performance comparison in different ways. For example, inflation in the Netherlands was much higher than in Finland. As a result, Dutch investors lagged significantly behind Finnish investors in terms of real returns, even though nominal returns are very similar”.

Finnish pension investors strong in regulated investor category

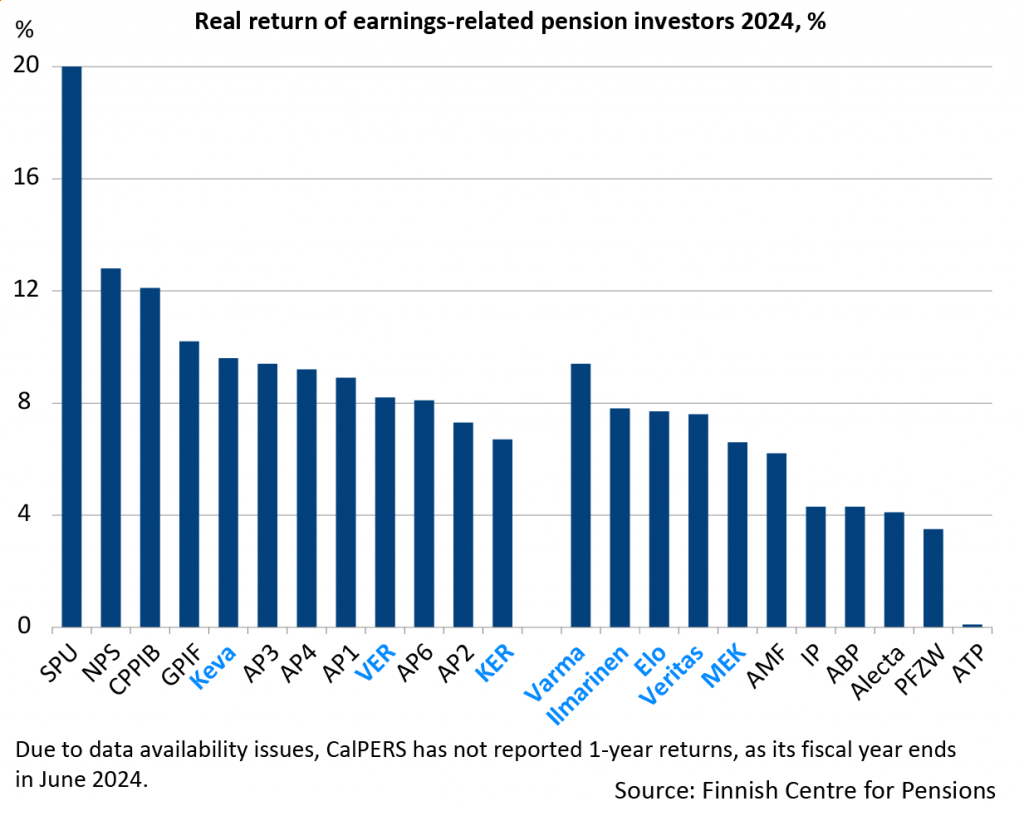

Finnish pension investors put in an impressive performance last year. In the category of regulated investors, Finnish pension investors took all the top spots. Varma, a Finnish pension fund, achieved the highest real return of more than 9 per cent. Ilmarinen, Elo and Veritas followed closely with real returns of just under 8 per cent.

Behind the Finnish pension investors were the Swedish occupational pension managers AMF and Alecta and the Danish funds IP and ATP.

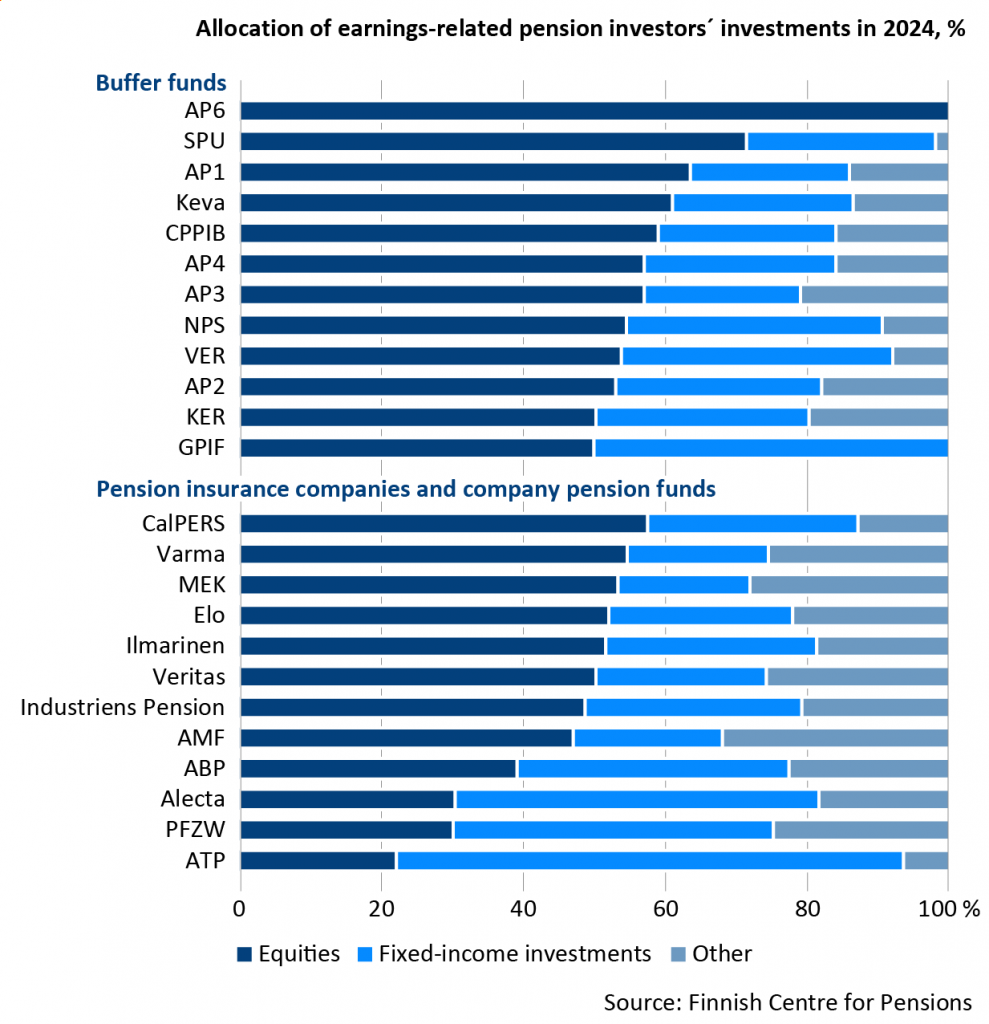

An important reason for the strong performance of Finnish pension investors appears to be the increased allocation to foreign equities in their portfolios. According to the Finnish Centre for Pensions, Finnish pension investors reduced the share of domestic stocks last year.

“Investing abroad paid off last year as the Helsinki Stock Exchange underperformed other markets,” says Special Adviser Antti Mielonen.

Among unregulated pension investors, Norway’s SPU buffer fund achieved the highest real return of 20 per cent.

“SPU’s return was mainly generated by equities, especially US technology companies. In addition, the continued depreciation of the Norwegian krone provided SPU with additional gains”, Mielonen adds.

South Korea’s statutory pension fund secured second place with a real return of almost 13 per cent. Among Finnish investors not subject to regulatory constraints, Keva returned 9.6 per cent and VER 8.2 per cent.

”Keva’s return was so strong that even Swedish buffer funds could not match it.”

Long-term real returns of 4-5 per cent

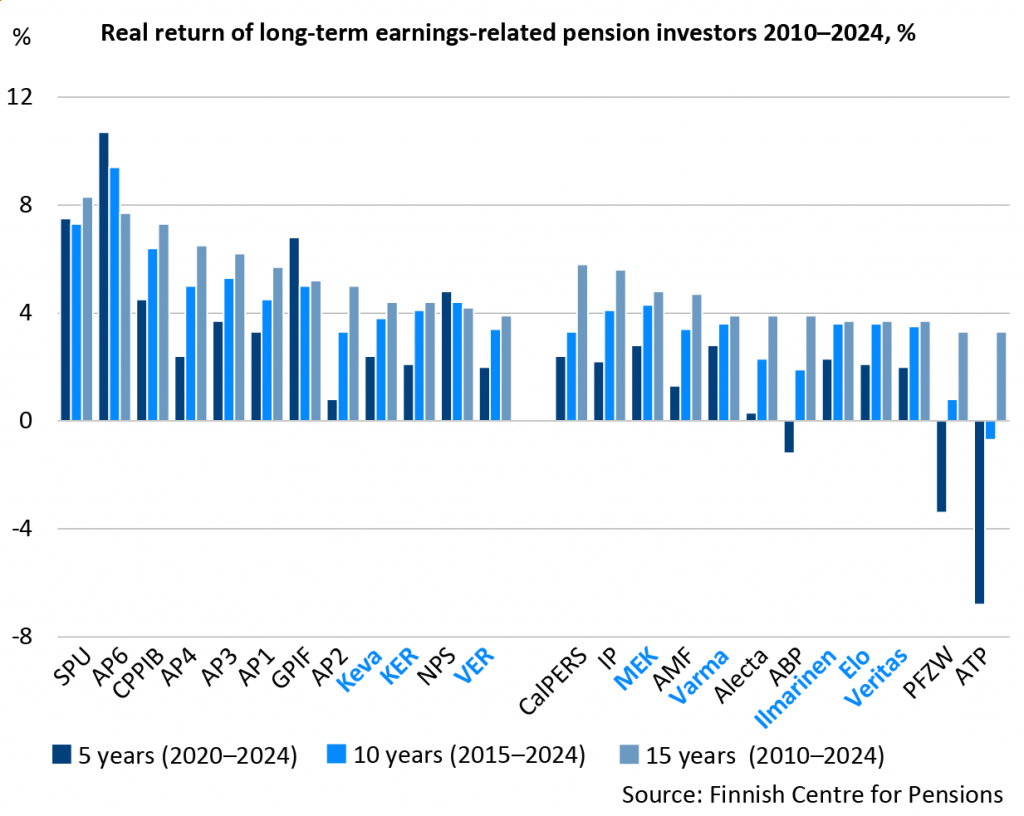

A long-term perspective smooths out the annual fluctuations in investment returns. Over a ten-year period (2015–2024), the average real return for pension investors is around 4 per cent. Over a fifteen-year period (2010–2024), the average real return rises to 5 per cent.

Among Finnish investors, the highest long-term real returns are achieved by the Seafarers’ Pension Fund (MEK), Keva and the Church Pension Fund (KER). The Seafarers’ Pension Fund has an average annual real return of 4.8 per cent over 15 years. The Church Pension Fund and Keva both have a real return of 4.4 per cent.

Finnish investment opportunities improve

Investment opportunities for Finnish private sector pension funds could become more yield- and risk-oriented in the coming years as their investment rules are updated. The new investment reform, agreed in January, means that private sector pension investors can allocate up to 85 per cent of their portfolio to equities.

Mika Vidlund of the Finnish Centre for Pensions says that such a high proportion of equities is unusually high by international standards.

“For example, Norway’s SPU can allocate a maximum of 72 per cent to equities. On the other hand, a high limit can help avoid the need to sell equities if their value rises sharply”.

Currently, Finnish private pension investors can allocate a maximum of 65 per cent of their portfolio to equities. A higher allocation to equities requires the investor to have a higher solvency capital.

At the turn of the year, just over half of Finnish pension investments were in equities. Most Finnish pension investors had just over a fifth of their allocation in bonds.

Pension investors divided into two groups

The Finnish Centre for Pensions’ investment return comparison covers 24 pension investors from Northern Europe, North America and Asia. The main investors from each country’s pension system, selected based on their coverage and investment assets, are included in the comparison. They are divided into two groups based on their risk-taking capabilities.

Investor-specific investment rules (buffer funds):

- Sweden: AP1-AP6 buffer funds

- Canada: Ganada Pension Plan Investment Board (CPPIB)

- Norway: Norwegian Government Pension Fund Global (SPU)

- Japan: Government Pension Investment Fund (GPIF)

- South Korea: National Pension Service (NPS)

- Finland: Keva, State Pension Fund (VER), Church Pension Fund (KER)

Subject to solvency regulations:

- USA: Californian Public Employees’ Retirement System (CalPERS)

- Netherlands: public-sector pension fund ABP and health care pension fund PFZW

- Sweden: Alecta and AMF Pension

- Denmark: ATP and Industriens Pension (IP)

- Finland: Earnings-related pension insurance companies (Elo, Ilmarinen, Varma, Veritas) and the Seafarers’ Pensions Fund (MEK).

Comparison criteria for investment returns

Solvency regulations and other risk-limiting investment policies set boundaries for investment activities.

The results are influenced by the starting year and the length of the comparison period. Even long-term average returns depend on the chosen timeframe.

Currency area and exchange rate fluctuations also affect the comparison. In the comparison of the Finnish Centre for Pensions, the returns are reported in the national currency, the same currency in which pensions are paid.

Real returns provide a more comparable picture of long-term returns by eliminating the impact of inflation.

Read more: