International comparison of investment returns: Inflation ate into Finn’s real returns

The investment year 2023 was challenging for pension funds in different parts of the world. The average real return of pension investors was less than 2 per cent. The yield of Finnish pension funds was even worse. Due to high inflation, the average real return 0.2 per cent negative. The average real return of Swedish pension funds was 1.2 per cent negative.

In a comparison conducted by the Finnish Centre for Pensions, 24 pension investors from nine different countries reached an average nominal return (after expenses) in 2023 of 8.2 per cent. However, inflation continued to be high, which is why the real return of the pension investors remained modest. The average real return shrunk to 2 per cent.

Finnish pension investors reached an average nominal investment return of 6 per cent.

“The nominal return was much better in 2023 than in 2022. But inflation was higher in Finland in 2023 than in many other countries, which clearly weakened the real return of Finnish pension investors”, explains Liaison Manager Mika Vidlund of the Finnish Centre for Pensions.

The real return of Finnish pension investors dropped to 0.2 per centnegative when inflation is measured with the average for the entire year 2023. The average real return in Finland in 2022 was 11.5 per centnegative.

“Nevertheless, the direction was good. Inflation dropped clearly in 2023, and after a weak year in 2022, the stock market was strong in 2023, particularly during the last quarter of the year.

Vidlund points out that our western neighbours have had a tough year, as well. The average real return of Swedish pension funds in 2023 was 1.2 per cent negative.

Best returns for Norwegian and Japanese pension investors

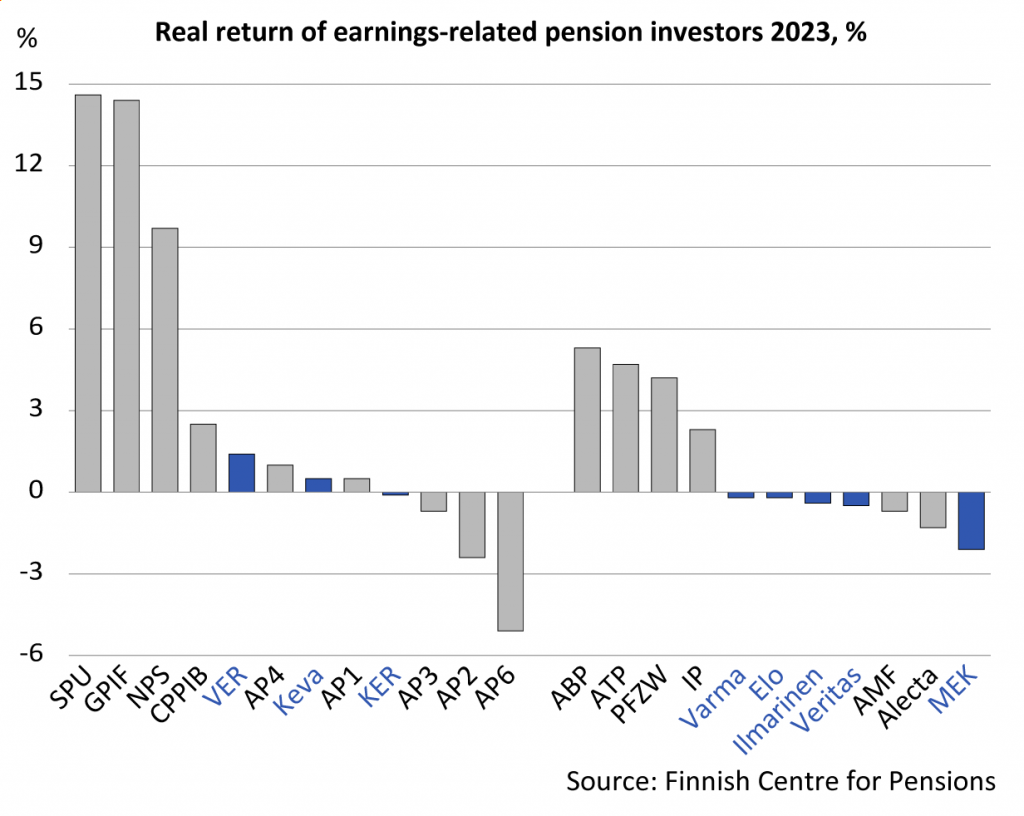

The three largest buffer funds reached the best return in the comparison conducted by the Finnish Centre for Pensions. The list is topped by the Government Pension Fund Global of Norway (SPU), the Government Pension Investment Fund (GPIF) in Japan and the National Pension Service (NPS) of South Korea.

Both SPU and GPIF reached a real return of over 14 per cent.

The Swedish buffer fund AP6, which specialises in capital investments, showed the weakest real investment return of 5.1 per cent negative.

Among the Finnish pension investors, the best real returns were achieved by The State Pension Fund of Finland (VER) and the municipal pension provider Keva. Both reached a slightly positive investment return. Private sector pension investors showed a negative real return.

“The Norwegian SPU did splendidly in 2023. Around 70 per cent of its allocation is in equities, half of them American. The AI rally in US technology stocks thus benefitted SPU directly”, Special Adviser Antti Mielonen estimates.

The exchange rate of the Norwegian krone also supported the success of the Norwegians, since the krone weakened in relation to the US dollar and thus improved the investments in dollars.

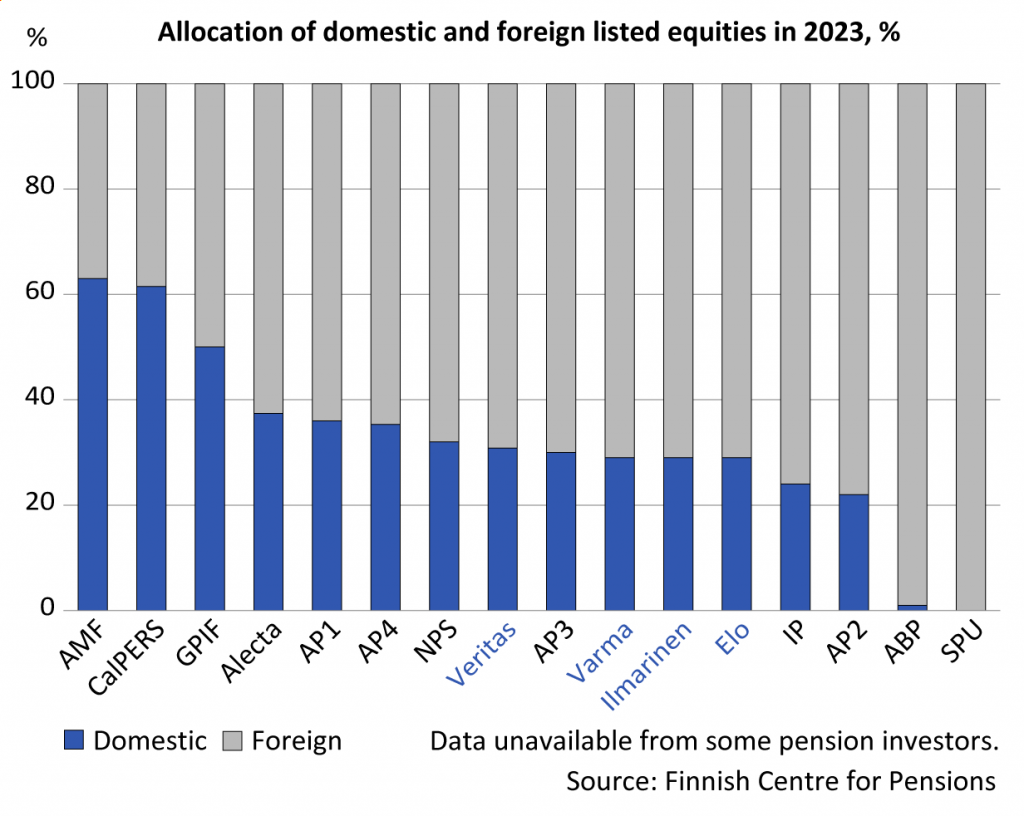

“SPU is a special case in that it does not hold any domestic equities. For Finnish pension investors, on the other hand, domestic equities accounted for almost one third of their stock market investments in 2023. The weak year of the Helsinki Stock Exchange no doubt affected pension investors’ returns”, Mielonen explains.

However, domestic equities may also surprise.

“For example, in Japan, investing in domestic equities turned out to be a good choice. The favourable return of the Japanese GPIF is explained by the top performance of domestic equities.”

Long-term real return 4–5 per cent

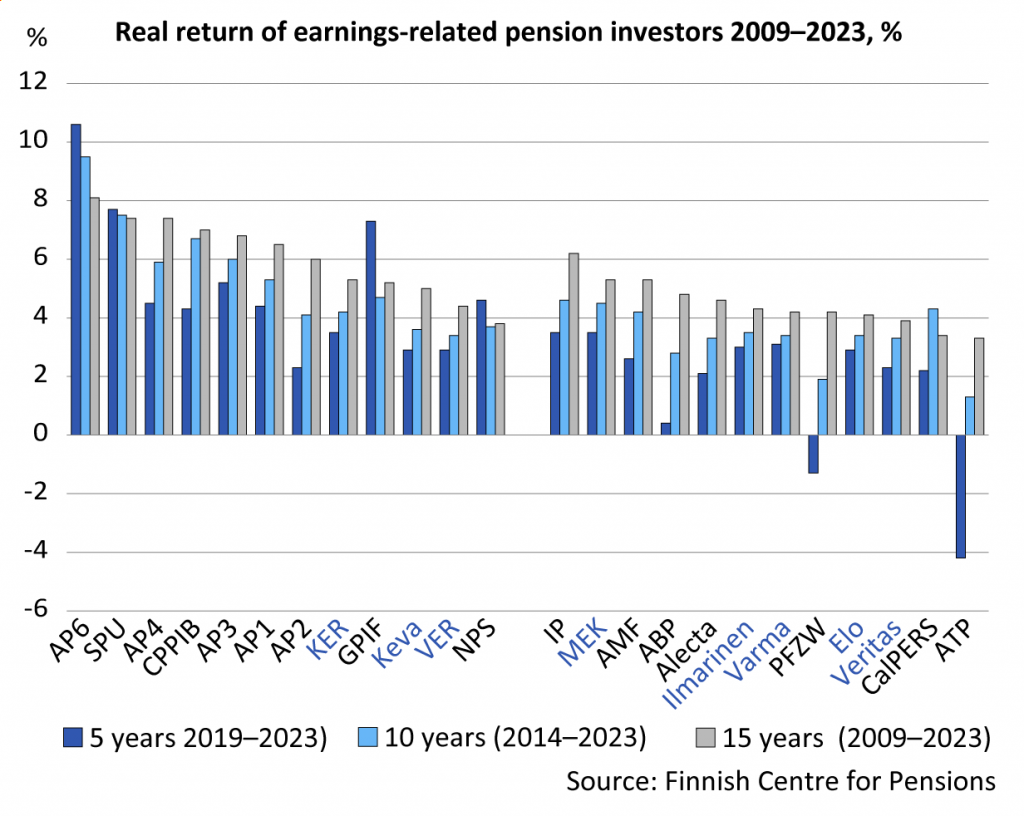

Pension investment has a long-term horizon and therefore it makes sense to monitor return rates over a longer period. The real return of pension investors over a period of ten years (2014–2023) is 4.4 per cent on average. Over a longer, 15-year-period (2009–2023), the average rate of return rises to 5.3 per cent.

Of the Finnish pension investors, the highest real return was achieved by the Seafarer’s Pensions Fund (MEK) and the Evangelical Lutheran Church of Finland (KER). The real return over the past 15 years for both pension investors was 5.3 per cent.

The return has also been affected by the expenses of investment operations. There are no harmonised data on expenses, but according to their financial statements, the foreign pension investors’ investment expenses in 2021–2022 were between 0.1 and 1.1 per cent of their investment capital. According to the Financial Supervisory Authority, the average investment expenses of the Finnish earnings-related pension investors in 2021 was 0.9 per cent of their investment capital.

Investment returns support pension financing

Finnish statutory earnings-related pensions are financed mainly through a pay-as-you-go (PAYG) system, that is, with the earnings-related pension contributions paid in the year in question. Yet, pension assets and their investment returns are used increasingly to finance pensions. In 2023, about 5.8 billion euros of pension assets were used to cover earnings-related pensions in payment.

Earnings-related pension investors divided into two groups

Our comparison of investment returns includes 24 pension sector providers from Northern Europe, North America and Asia. They are all major pension investors in their respective pension systems, both in terms of coverage and investment assets. The earnings-related pension investors are divided into two groups in the comparison based on their risk-bearing capacity.

Buffer funds with actor-specific investment regulations:

- Swedish buffer funds (AP1-AP6),

- the Canada Pension Plan Investment Board (CPPIB),

- the Norwegian Government Pension Fund Global (SPU),

- the Japanese Government Pension Investment Fund (GPIF),

- the National Pension Service of Korea (NPS), and the Finnish pension funds:

- Keva,

- the State Pension Fund (VER), and

- the Church Pension Fund (KER).

Investors who are subject to solvency regulation:

- the California Public Employees’ Retirement System (CalPERS),

- the Stichting Pensioenfonds (ABP) and the Pensioenfonds Zorg en Welzijn (PFZW) of the Netherlands,

- the Swedish occupational pension funds Alecta and AMF,

- the Danish occupational pension fund ATP,

- the Finnish earnings-related pension insurance companies (Elo, Ilmarinen, Varma, Veritas) and the Seafarers’ Pension Fund (MEK).

Boundary conditions for comparison of investment returns

- Starting year and length of comparison period affect the results. Substantial annual fluctuation in returns. Long-term average returns depend on the selected period.

- Currency region and exchange rate fluctuations cause differences in results. Returns expressed in national currency (that is, in the same currency as that in which the pensions are paid).

- Investment operations take place within the solvency framework and other regulations limiting investment risks.

- Real returns provide better comparability of long-term investment returns as the effect of inflation is removed. Calculations of real return use the average value of OECD Stat’s Consumer Price Index (CPI) for the investment year. It depicts the impact of inflation for the whole year.

Read more on Etk.fi: