Working in Retirement

Working in retirement in 2023 at the same level as in 2022

At year-end 2023, nearly 1,5 million persons received a pension paid based on their own working life. One in ten of them worked. One in four under the age of 68 worked.

There were more than 180,000 pensioners who worked throughout the last year. Of them, 100,000 were under 68 years of age. They were covered by the obligation to insure and thus earned a new pension for their work. If almost 50,000 insured persons who worked while drawing a partial old-age pension in 2023 are added to the figures, the number of persons working in retirement is 230,000.

Type of pension benefit affects the number of people working

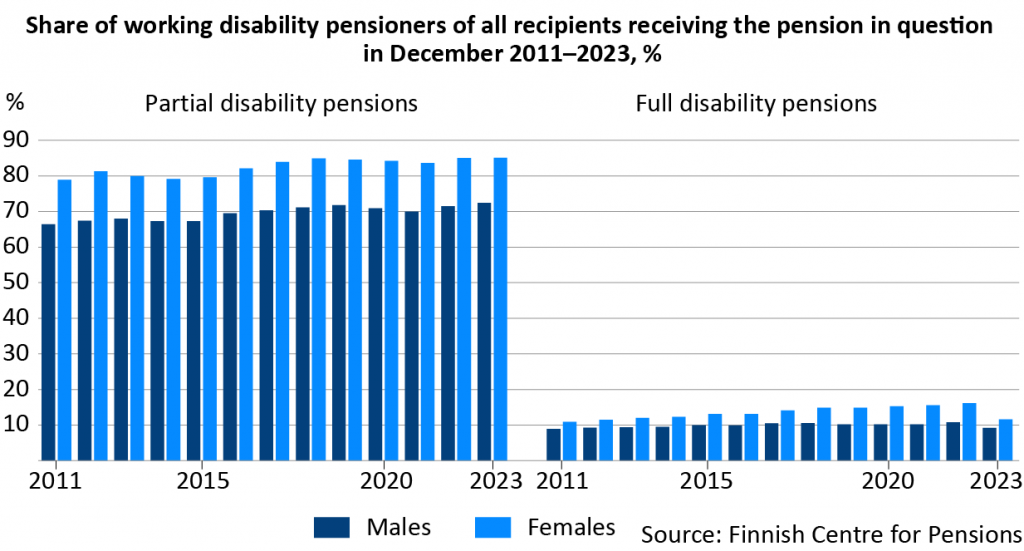

Working is most common among those who receive a partial disability pension: as many as 81 per cent of them worked at year-end 2023. Working is also common among people drawing a partial old-age pension. At the end of 2023, three in four recipients of the partial old-age pension continued to work.

At the end of 2023, there were more than 1.3 million old-age pensioners in Finland, of whom 84,000 worked. Of those who received a full old-age pension and were under the age of 68, around 32,000 worked in 2023. Just under 3,000 of them were under the age of 64.

Number of pension recipients working in December 2023 and share of recipients of pension in question

| Pension benefit | Under 68 year-olds, persons | Under 68 year-olds, % | All, persons | All, % |

|---|---|---|---|---|

| All | 101,900 | 24.7 | 153,200 | 10.3 |

| – Excl. the partial old-age pension | 59,400 | 16.7 | 110,700 | 7.8 |

| Full old-age pension | 32,300 | 13.4 | 83,600 | 6.4 |

| Partial old-age pension | 42,400 | 75.2 | 42,500 | 75.2 |

| Disability pension | 27,100 | 23.7 | 27,100 | 23.7 |

| – Full disability pension | 9,600 | 10.4 | 9,600 | 10.4 |

| – Partial disability pension | 17,500 | 81.1 | 17,500 | 81.1 |

Change of statistical method reduced the number of people under age 68 who worked in retirement

In the data for 2023, the criteria for statistics were changed. The data excluded, among other things, low earnings from work. As a result of this change, the number of pensioners working in retirement decreased compared to before. The income limit decreased the number of pensioners working, especially the number or those who work while receiving a full disability pension, as they can only work a little without losing their pension.

Without the change, the number of persons working in retirement in 2023 would have been on level with the number in 2022. In fact, the percentage of those receiving a certain pension would have increased slightly. Overall, the impact was half a percentage point for pensioners aged under 68, but the differences between pension types were much larger.

Pensioners who worked during the year

As many pensioners work part-time and perhaps not very regularly, there were significantly more pensioners who worked during the year than in December. On average, old-age pensioners under 68 worked for just over six months in 2023. With age, earnings and the number of working months decreases. For example, 70-year-old pensioners worked on average for just over five months and 75-year-olds for four months.

Number of pension recipients working in 2023 or in December 2023, average pension and average earnings

| Working and retired | All pension benefits | All pension benefits, excl. partial old-age pension | Full old-age pension | Old-age pension, under 68 |

|---|---|---|---|---|

| Working and retired in December, persons | 153,200 | 110,700 | 83,600 | 32,300 |

| – Pension €/month | 1,740 | 2,110 | 2,410 | 2,100 |

| – Wage €/month | 2,270 | 1,730 | 1,760 | 1,980 |

| During the year, working and retired, persons | 234,000 | 182,800 | 141,500 | 60,500 |

| – Pension €/month | 1,810 | 2,090 | 2,310 | 1,980 |

| – Wage €/month | 2,080 | 1,650 | 1,640 | 2,050 |

Working while drawing a pension has increased steadily since 2007. Both the number of persons and the share of persons under 68 years has increased. Part of the increase can be explained by the growing number of persons drawing a partial disability pension while part of it stems from the fact that working while drawing an old-age pension has become more common. Drawing a partial old-age pension has also raised the number of working pension recipients considerably as of 2017 although persons receiving a partial old-age pension are not counted as pensioners as such.

The part-time work of pensioners also affects the income earned from work. For example, the average earnings from work of persons receiving an old-age pension is lower than their average pension, which indicates a clear drop in the earnings level from the level before retirement.

The temporary nature of work done while drawing a pension is also reflected in the variation in the number of persons working over the year. When slightly more than 150,000 persons receiving a pension in December 2023 worked, they numbered nearly 80,000 more over the entire year, that is, more than 230,000 persons in total. The figures include 50,000 partial old-age pension recipients, a significant proportion of whom worked.

Getting an extra income is not the primary incentive for working in retirement. The earnings level and the temporary nature of working, as well as research conducted on this subject, support this conclusion. In addition, the old-age pensions of working pension recipients are higher, on average, than the old-age pensions of others of the same age.

Working more common among women under 68 than men

Working is more common among women under 68 than men. At year-end 2023, more than 55,000 women drawing a pension worked, while the equivalent figure for men was 47,000.

When the partial old-age pension is excluded from the review, less than 24,000 (or 13.9%) retired men under the age of 68 worked. For women, the corresponding figure were 35,400 (19.4%).

If older age groups are also included, the picture of the prevalence of work between the sexes changes. Men’s work is more common in people over the age of 70. It raises the proportion of working pensioners among men by a couple of percentage points higher than that of women.

Number of pension recipients working in December 2023 and share of recipients of this pension benefit, by gender

| Pension benefit | Males, persons | Males, % | Females, persons | Females, % |

|---|---|---|---|---|

| All | 76,100 | 11.3 | 77,100 | 9.5 |

| – Excl. partial old-age pensions | 53,500 | 8.3 | 57,200 | 7.3 |

| Full old-age pension | 44,200 | 7.5 | 39,400 | 5.4 |

| Partial old-age pension | 22,600 | 72.4 | 19,900 | 78.6 |

| Disability pension | 9,300 | 17.1 | 17,800 | 29.6 |

| – Full disability pension | 4,400 | 9.2 | 5,300 | 11.6 |

| – Partial disability pension | 4,900 | 72.4 | 12,600 | 85.1 |

The gap in the number of men and women receiving a partial disability pension is particularly wide. This pension benefit is considerably more common among women than men. In line with the goals of this pension benefit, most persons drawing a partial disability pension continue working while drawing the benefit. Of women drawing a partial pension at year-end 2023, roughly 85 per cent worked. For men, the share was more than 10 percentage points lower.

More than 80,000 persons receiving a full old-age pension worked

Of those who received a full old-age pension, 84,000 (6.4%) worked in December 2023. Of them, over 32,000 were under the age of 68. When all those who worked alongside the old-age pension in 2023 were included, there numbered more than 140,000.

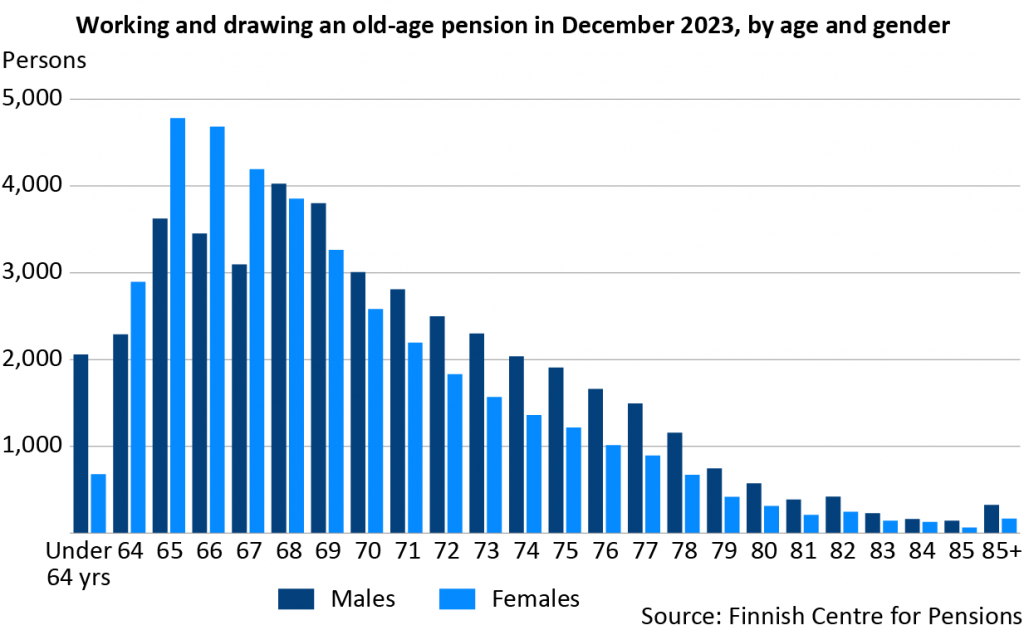

The number of people working while drawing an old-age pension decreases with age. Young old-age pensioners work more than older ones. Most of them are women. The older the age groups, the smaller the proportion of those alive in that age group are men. However, most pensioners working in older age groups are men.

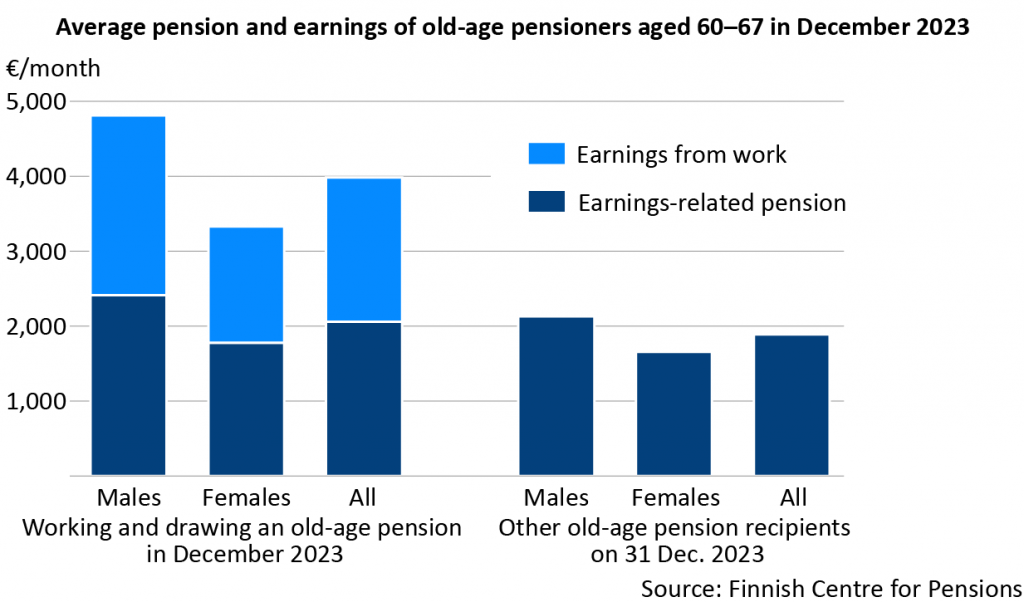

In December 2023, more than 31,000 people aged 60 to 67 worked while receiving a full old-age pension. The average combined monthly income from work and old-age pension of retired med in this age group rose to 4,900 euros. For women, the average income was just under 3,600 euros. Working doubled the monthly income of old-age pensioners in the months they worked. The higher-than-average old-age pensions of working pensioners indicates that the incentive for them to work is not primarily financial.

Although the earnings-related pension of working old-age pensioners is reasonably high on average, it is low for some. In December 2023, the earnings-related pension of 7 per cent (6,300 persons) of working old-age pensioners received a pension that was less than the limit for the guarantee pension (€922/month). Two in three were women. Just over half of those under the limit were under 70 years of age. It is also worth remembering that many of the members of this group receive not only an earnings-related pension but also a national pension, which is excluded from this review.

43,000 disability pensioners worked

Working is possible also while drawing a disability pension. The number of working disability pensioners has clearly risen during the last decade. In 2023, 43,000 insured persons worked alongside the disability pension, of which more than 27,000 worked in December.

Working is particularly common among persons drawing a partial disability pension – this applies to four in five partial disability pensioners. In December 2023, they numbered 17,500, of whom 12,600 were women. Of those working while drawing a partial disability pension, slightly more than half were under the age of 60.

Working is less common among those who draw a full disability pension, but even they can do some work. In December 2023, working full disability pensioners numbered more than 21,000 (slightly less than 10,000 in December), of whom just over half were women. Two in three were aged under 60.

The average monthly part-time pension in December 2023 was just over 900 euros and the average monthly earnings from work 1,900 euros. Correspondingly, the average pension of those receiving a full disability pension was 1,600 euros and the average monthly earnings 1,200 euros per month of work. Working increases the total income of persons receiving a full disability pension and persons receiving a partial disability pension to the same level.

Cause of disability affects employment opportunities alongside retirement

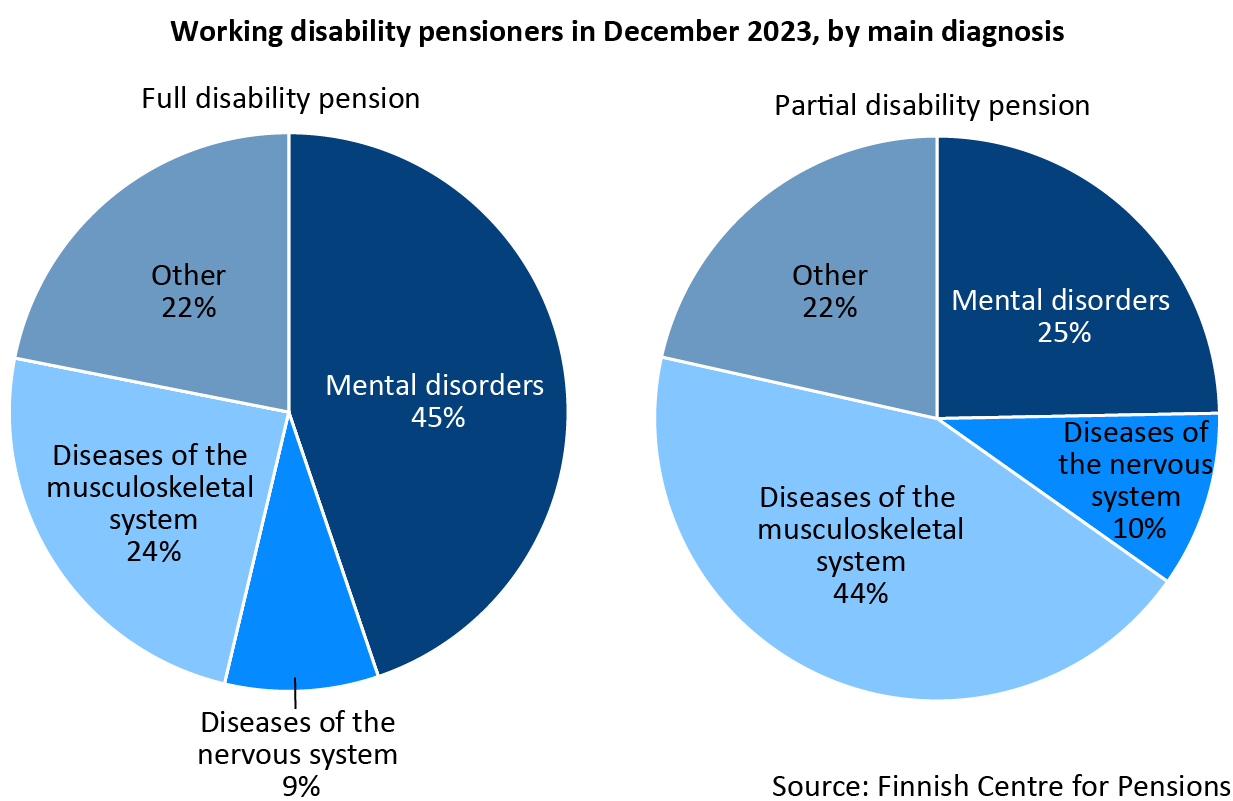

Nearly half of all recipients of a full disability pension who worked at year-end 2023 were granted the disability pension because of mental disorders. Every fourth received the pension due to musculoskeletal disorders. For the partial old-age pension, the situation is the opposite: nearly half worked despite musculoskeletal disorders. Every fourth working partial disability pension recipient suffered from mental disorders. For the other main groups of diseases, the differences were small.

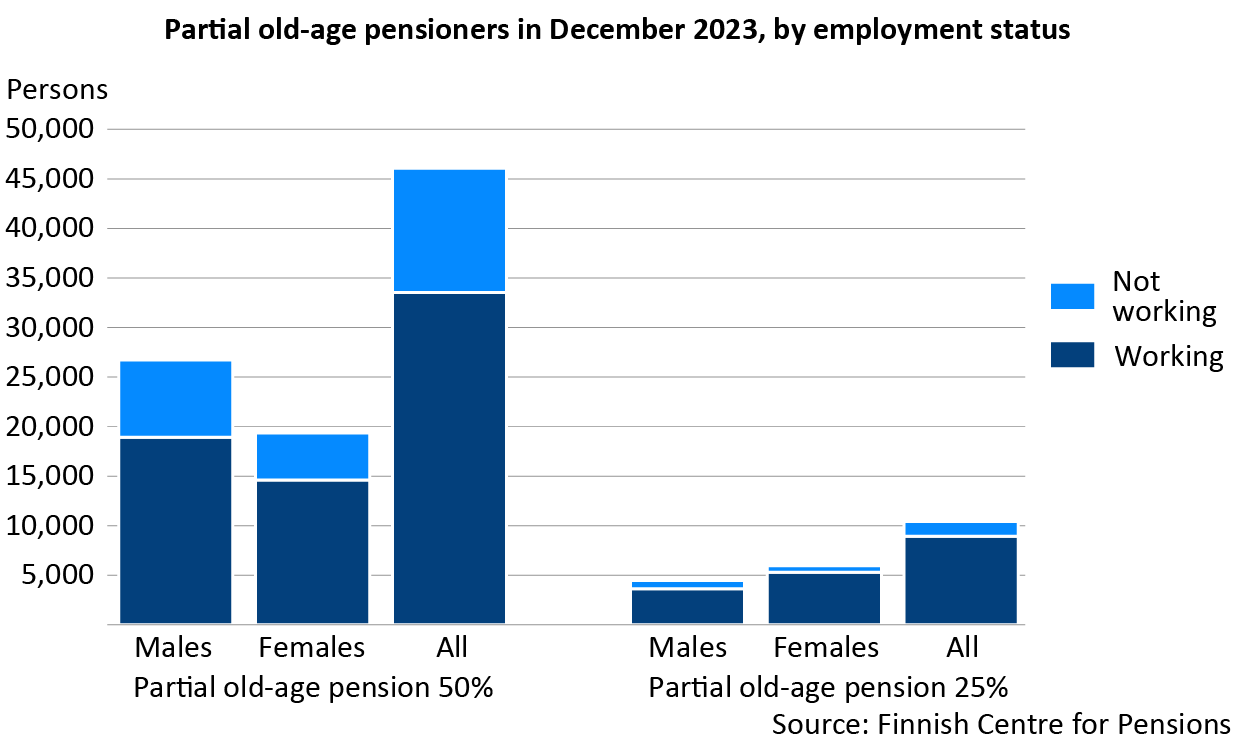

Majority of partial old-age pension recipients continue working

At year-end 2023, more than 56,000 persons insured for an earnings-related pension received a partial old-age pension. The partial old-age pension can be granted at age 61. A person can take out one quarter or half of the pension they have accrued by the time they start drawing the partial old-age pension. Most have selected to take out 50 per cent of their accrued pension.

Most persons receiving a partial old-age pension worked at year-end 2023. Three in four persons selecting to draw a 50-per-cent partial old-age pension continued to work, and nearly 86 per cent of those drawing a 25-per-cent partial old-age pension were working.

It is no surprise that the share of working partial old-age pensioners is large. In practice, the pension received is less than half of the accrued pensions, which is seldom enough to live on. At year-end 2023, the average monthly pension of those working and drawing a 50-per-cent partial old-age pension was 870 euros. For those drawing a 25-per-cent pension, it was half of that. In addition to their pension, men received average monthly earnings from work of 4,100 euros and women 3,200 euros.

Following the 2017 pension reform, the partial old-age pension replaced the part-time pension which required that the pension recipient continued working. The pension benefit still encourages older people to continue working. When it is possible to reduce the work load towards the end of one’s working career with the help of the partial old-age pension without having to considerably compromise one’s standard of living, it can help people continue working for a longer time.

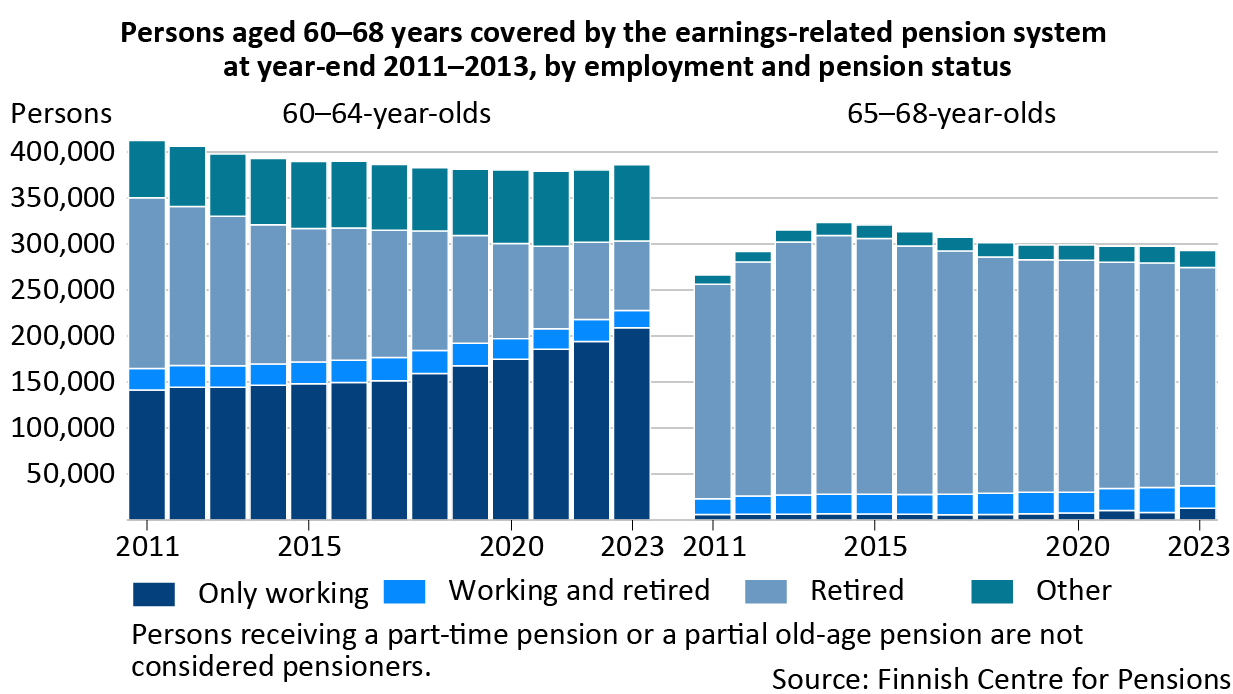

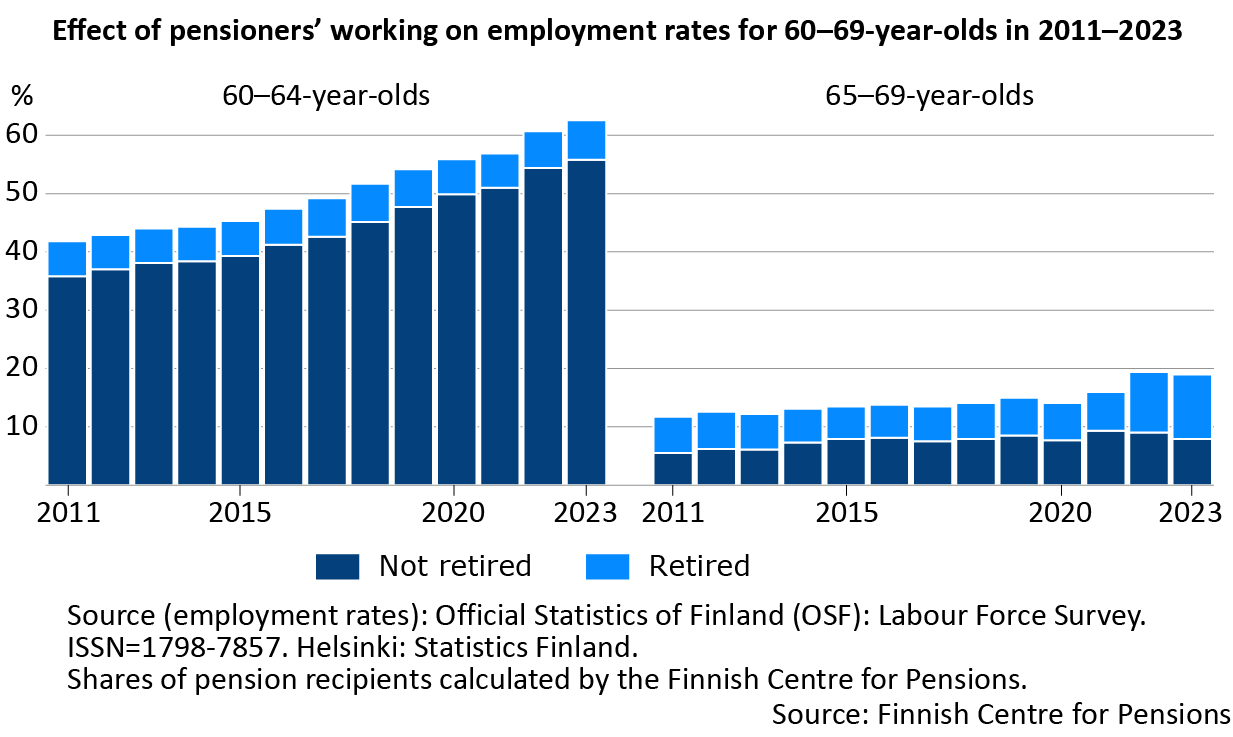

Working in retirement raises the employment rate among older people

At year-end 2023, around 230,000 insured persons between the age of 60 and 64 were working. This corresponds to 60 per cent of the age group covered by the earnings-related pension scheme. Since 2011, the percentage has risen by 20 percentage points, that is, by 63,000 insured persons. While the number of pension recipients has fallen in this age group, the share of those who have worked while drawing a pension has remained around five percentage points. In other words, the number of persons working has risen mainly among those who were not retired. Here, this group includes those who have received a partial old-age pension.

Work among 65 to 68-year-olds has also become more common over the period 2011-2023. At the end of 2023, just under 40,000 insured persons worked, two in three of whom were pension recipients.

As working among those of a pensionable age and those who have retired becomes more common, the employment rate among older people rises. For example, in the age group 65–69-year-olds, more than half of the employment rate in 2023 can be contributed to working pensioners. In addition, around 3,400 persons in this age group worked while receiving a partial old-age pension in December 2023.

Correspondingly, every tenth person in the age group 60–64-years who were working was a pension recipient. If the recipients of a partial old-age pension were considered as pensioners, the share of pension recipients in this age group would nearly double.

(Updated on 24 January 2025)

Statistical tables:

Statistical services provides further information:

Working in retirement

Producer: Finnish Centre for Pensions

Website: https://www.etk.fi/en/research-statistics-and-projections/statistics/working-in-retirement/

Subject area: Work, wages and livelihood

Part of the Official Statistics of Finland (OSF): No

Description

These statistics describe pensioners’ pension-insured work in retirement and their average income and earnings-related pensions. The material is divided into two groups based on age. The second set consists of all earnings-related pension recipients. A subset of the population is persons under the age of 68 who are covered by the obligation to insure and thus increase the new pension.

Data content

The statistics contain information on working in retirement among the working-age population. Working is examined in terms of number of people, population shares and changes over time. The data includes information on pensioners’ average pensions and earnings.

Categorizations

Gender, age, pension benefit, main disease category

Methods of data collection and source

The data on working in retirement are based on the data in the earnings and pension registers of the earnings-related pension system. For pensioners exceeding the age when the insurance obligation ends (68 years), the data has been combined with the Tax Administration’s data on income subject to withholding tax. Data on employment rates are based on Statistics Finland’s Labour Force Survey.

Update frequency

Once a year.

Time of completion or release

The statistics is released at the end of the year following the statistical year. The exact date of publication is stated in the release calendar.

Time series

The time series for the statistics starts from 2007.

Key words

pensioners, working, continued working, gainful employment, employment rate, older workers, earnings-related pensions

Contact information

Concepts relating to work

Earnings-related pension scheme

The statutory earnings-related pension scheme is divided into the private and the public sector.

Most persons working in the private sector are insured under the Employees Pensions Act.

As a rule, persons working in the public sector are insured under the Public Sector Pensions’ Act. The act covers persons working for Keva’s member companies, the State, the Evangelical-Lutheran Church and the Social Insurance Institution of Finland (Kela). Most persons insured in the public sector work in the municipal sector.

Insured under the earnings-related pension acts, insured

A person who, at the time of compiling the statistics or previously, were in an employment relationship or worked as a self-employed person, and who is eligible for an earnings-related pension at the time of the pension contingency.

Work insured under the earnings-related pension acts

Work done between the ages of 17 and 67 must be insured under an earnings-related pension act. The obligation to take out insurance ends when the person turns 68 years and concerns earnings that exceed a certain monthly limit (€65.26/month in 2023). If a retired person works, their earnings must also be insured, and they earn new pension for those earnings.

Since the obligation to take out insurance ends at the end of the month in which a person turns 68, part of the reviews has been limited to persons aged 67.

Self-employment insured for earnings-related pension

Self-employment must be insured if the annual earnings from self-employment is at least 8,575 euros (in 2023). Self-employment carried out by a pension recipient must also be insured. The only exception are self-employed persons who have retired on an earnings-related old-age pension. They are not under obligation to take out pension insurance under the Self-employed Persons’ Pensions Act, but they may take out voluntary insurance under the Self-employed Persons’ Pensions Act. That is why some of the self-employed persons on a pension are excluded from this data even though they continue working as self-employed persons.

Self-employed persons covered by mandatory and voluntary pension insurance under the Self-employed Persons’ Pensions Act are considered working people. A self-employed person as referred to in the Self-employed Persons’ Pensions Act is a person who engages in gainful employment without being in a service or an employment relationship. A self-employed person’s family member is also a self-employed person if they work in the company but is not in an employment relationship in that work.

Under the Farmers’ Pensions Act, pension insurance must be taken out for annual earnings of at least 4,288 euros (in 2023). Insurance under the Farmers’ Pensions Act must be taken out if the person farms on an estate of at least five hectares and does the work themselves. The insurance obligation also applies to family members whose main work is done on the farm.

As of 2009, grant recipients who engage in scientific research or artistic activities are also covered by the Farmers’ Pensions Act.

Activities covered by the Farmers’ Pensions Act by a pensioner can also be insured if the requirements of the Act are met.

Person in employment

A person who has been working during the calendar month for which pension has accrued or insured for earnings-related pension based on activities covered by the Self-employed Persons’ Pensions Act or the Farmers’ Pensions Act.

Persons who have reached the age when the insurance obligation ends and who, according to the Tax Administration’s withholding tax data, have received earnings that exceeded the lower limit of the obligation to insure younger age groups (see previously “Work insured for earnings-related pensions”).

Person in employment at year-end

A person who has worked in December or at year-end (depends on how the working is reported). This causes slight differences in the statistics regarding numbers at the end of the year.

Concepts relating to pensions

Retired

A person who receives an earnings-related pension based on their own working life. Although people who draw a partial old-age pension are not considered retired, they are considered retired in this statistics.

Disability pension

A disability pension may be granted to persons between the ages of 17 and 64 whose ability to work has been reduced due to an illness and whose inability to work is estimated to last for at least one year. A full disability pension is paid if the ability to work has been reduced by at least 3/5. A partial disability pension is paid if the ability to work has been reduced between 2/5 and 3/5.

The disability pension can be granted as a temporary rehabilitation allowance or a pension valid until further notice, in which case it has not been determined when it will end. A temporary disability pension (also called a cash rehabilitation benefit) is a fixed-term disability pension that can be granted when the rehabilitee’s ability to work is expected to improve because of treatment or rehabilitation. The temporary disability pension can also be granted to the amount of the partial pension. The temporary disability pension is here counted as a disability pension.

The disability pension may be awarded either to the amount of a full pension or a partial pension. A person drawing a disability pension has the right to work within the scope of their remaining work ability. When drawing a full disability pension, the earnings from work must be less than 40 per cent of the stabilised average earnings. A full disability pension is converted into a partial disability pension if the earnings from work exceed 40 per cent but are no more than 60 per cent of the stabilized income level before drawing a disability pension. Pension payments may be interrupted if the earnings exceed the earnings limits.

Old-age pension

A person can retire on an old-age pension flexibly between the ages 63 and 68 when they stop the work from which they retire. In 2022, the age limit rose to 64 years. In addition to the general rule, there are certain exceptional groups of people in the public sector who can retire on an old-age pension before reaching their retirement age. Such groups are, for example, employees of the armed forces.

Drawing an old-age pension does not prevent the recipient from working, nor does the income earned in retirement affect the payment of the pension. Pension for work done in retirement is granted at the age of 68 at the earliest.

The partial old-age pension replaced the part-time pension in 2017. Taking out a partial old-age pension does not require that the employment relationship is terminated, so in these statistics, persons on a partial old-age pension are not considered people who have retired on an old-age pension. However, they are included in the tables on all pension recipients. Data on recipients of the partial old-age pension have also been tabulated separately.

Other concepts

Age

Person’s age at end of year under review Working-aged or active-aged people refer in this connection to 17–67-year-olds. At this age interval, work must be insured for an earnings-related pension. The employment data is entered into the registers of the earnings-related pension system.

People who can select to retire on an old-age pension refers to people aged between 63 and 67 and, as of 2022, to people aged between 64 and 67. In that age interval, it is possible to select when to retire.

Working while drawing a pension

People working in retirement are interpreted as people who receive some type of earnings-related pension benefit based on their own working life while simultaneously working and earning new pension for that work. Since a pension is always paid for the whole calendar month, working for just one day in the same month is working while drawing a pension.

For the first time, the 2023 dataset also contains data on work carried out after reaching the age when the insurance obligation ends. In this respect, the data are based on the Tax Administration’s withholding data, which are based on the declarations of withholdable income made by employers and other payers to the Incomes Register for general taxpayers.

With the new data, the criteria for statistics were also changed in the 2023 statistics. For example, minor earnings were excluded from the material when the earnings limit was set at 65.26 euros per month in 2023. As a result of the change in the statistical method and principles, the number of pensioners employed fell compared to the previous one. For example, the income limit decreased the number of pensioners working, especially the number or those who work while receiving a full disability pension, as they can only work a little without losing their pension.

Without the change, the number of persons working in retirement in 2023 would have been on level with the number in 2022. In fact, the percentage of those receiving a certain pension benefit would have increased slightly. The decrease in the number of persons from the previous year is therefore due to the change in the statistical method. Overall, the impact was half a percentage point for pensioners aged under 68, but the differences between pension types were much larger.

Although the change in the statistical concept causes a break in time series, coverage is improved. The revised statistics also contain data on the work of those who have passed the age when the insurance obligation ends. In 2023, they included all those over the age of 68. The number of persons employed is not small; in December 2023 it increased the number of persons who worked alongside the old-age pension by 50,000.

The long-term objective of the Finnish Centre for Pensions has also been to obtain information on work carried out after the age when the insurance obligation ends. In the 2023 datasets, the target was realised when the data from the Tax Administration were also combined with the register data. At the same time, the concepts were changed and harmonised.