Current information on pensions and taxation

The amount of the net pension is affected by how the earnings-related and national pension benefits and the taxation of pensions are determined. Earnings-related pensions rose by 0.9 per cent by the earnings-related pension index at the beginning of 2026. The monthly amount of the national pension and the guarantee pension was increased by the national pension index, that is, by 0.5 per cent. The index adjustments to the housing allowance for pensioners are frozen for the period 2024–2027.

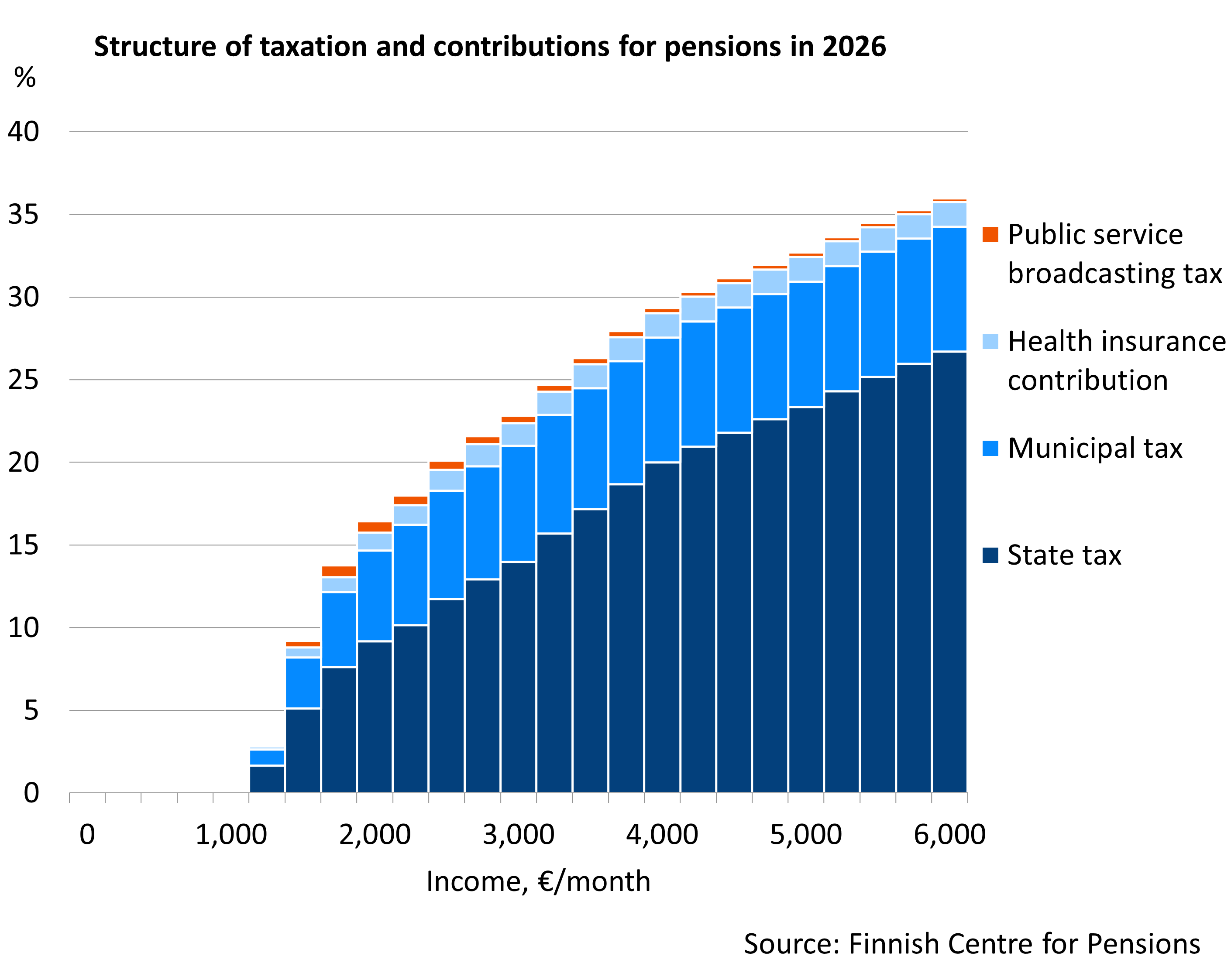

In 2026, the tax burden on pensioners is slightly reduced in lower incomes by the increases in the basic deduction and the pension income deduction. The deductions mean that low-income pensioners pay no municipal tax on annual pension earnings of less than 13,905 euros (€1,159/month). The right to the pension income allowance extends to annual earnings of 49,315 euros (€4,110/month).

Full amount of pension income deduction and annual income limit as of which the pension recipient starts to pay tax, as well as annual income limit as of which no deduction is granted (in 2026)

| Full deduction, €/year | Pension amount as of which tax becomes payable, €/year | Pension amount for which no deductions are granted, €/year |

|---|---|---|

| 11,080 | 13,905 | 49,315 |

In 2026, the average municipal tax rate is 7.57 per cent. The public broadcasting tax is 2.5 per cent for an annual income that exceeds 15,150 euros (but 160 euros at most). The health insurance contribution payable on pension and benefit income is 1.49 per cent. The additional pension income tax paid to the State is 5.85 per cent for pension income exceeding 60,000 euros per year (€5,000 per month). The income threshold for the additional tax was increased from the previous €47,000.

The net pension of a person who is paid a pension only from Kela will rise in 2026 by 0.5 per cent compared to 2025 because of increases in the national and guarantee pension indexes. The net pension in higher income brackets rose by 0.7–1.6 per cent.

Around one third of pensioners have a monthly pension of less than 1,500 euros and therefore pay less than nine per cent in tax. One quarter of pensioners have a pension of over 2,500 euros, at which income level the tax rate rises to over 20 per cent. Just under 6 per cent of pensioners have a pension of over 4,000 euros, on which they pay more than 29 per cent in tax.

More on other sites:

- Total pension in Finland 2025: How are earnings-related pensions, national pensions and taxation determined? (Julkari.fi)

- Tax percentage calculator (Vero.fi)

Taxes and contributions on wage and pension

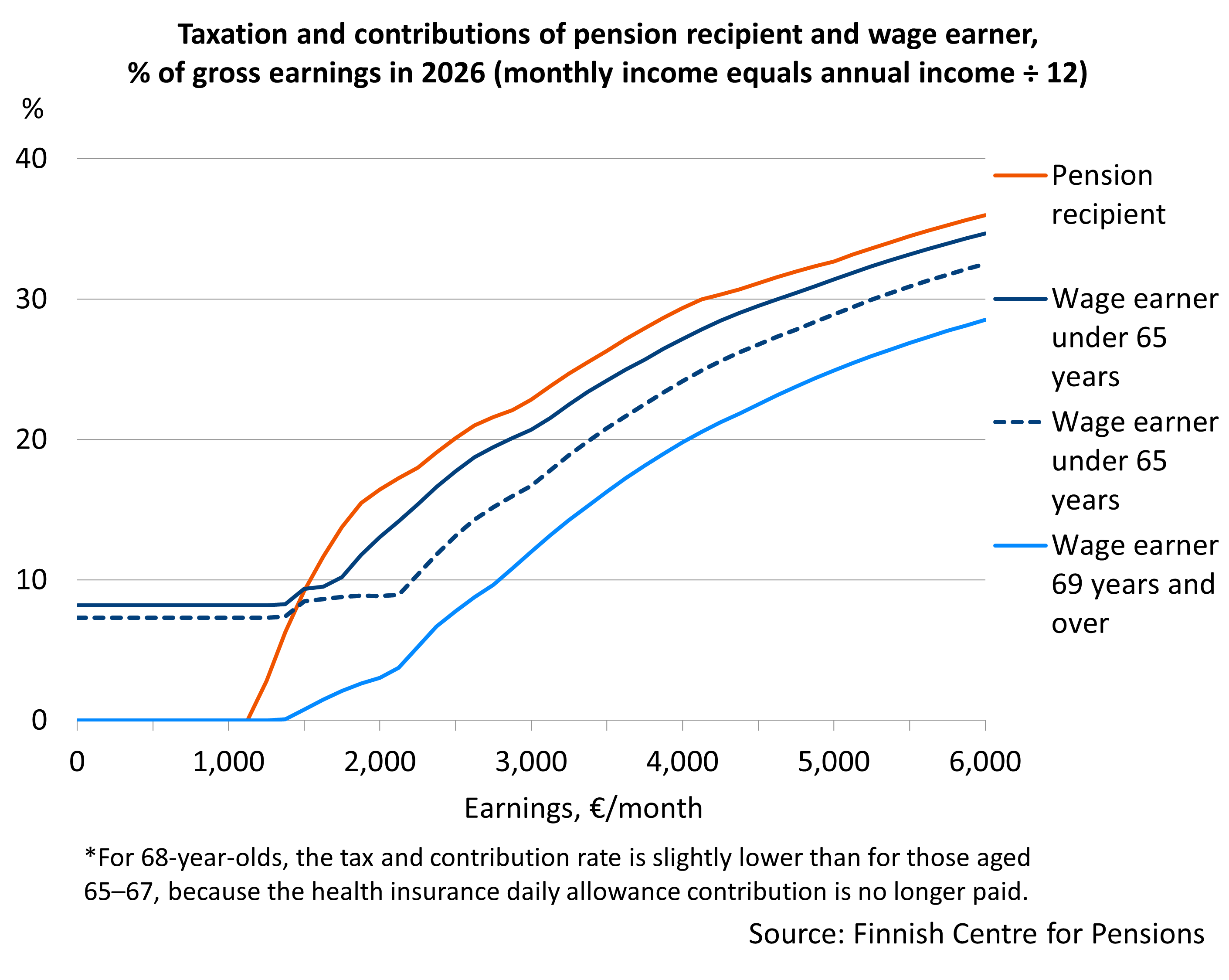

In the figure below, the tax and contribution burdens of wage earners and pension recipients in 2026 are compared at different income levels (monthly income is the annual income divided by 12). The total contribution rate is different for wage earners of different ages since the contributions change based on age. A person aged 69 or more no longer pays contributions for wage-earners. The earned income deduction is increased for those aged 65 and over. With monthly earnings of around 1,500 euros or more, the tax and contribution burden of pension recipients is a couple of percentage points higher than that of wage‑earners under 65 years. The difference is largest at a monthly income of 1,800 euros, at around 3.5 percentage points. When income exceeds 5,000 euros, the difference narrows to around one percentage point.

Development of net pension

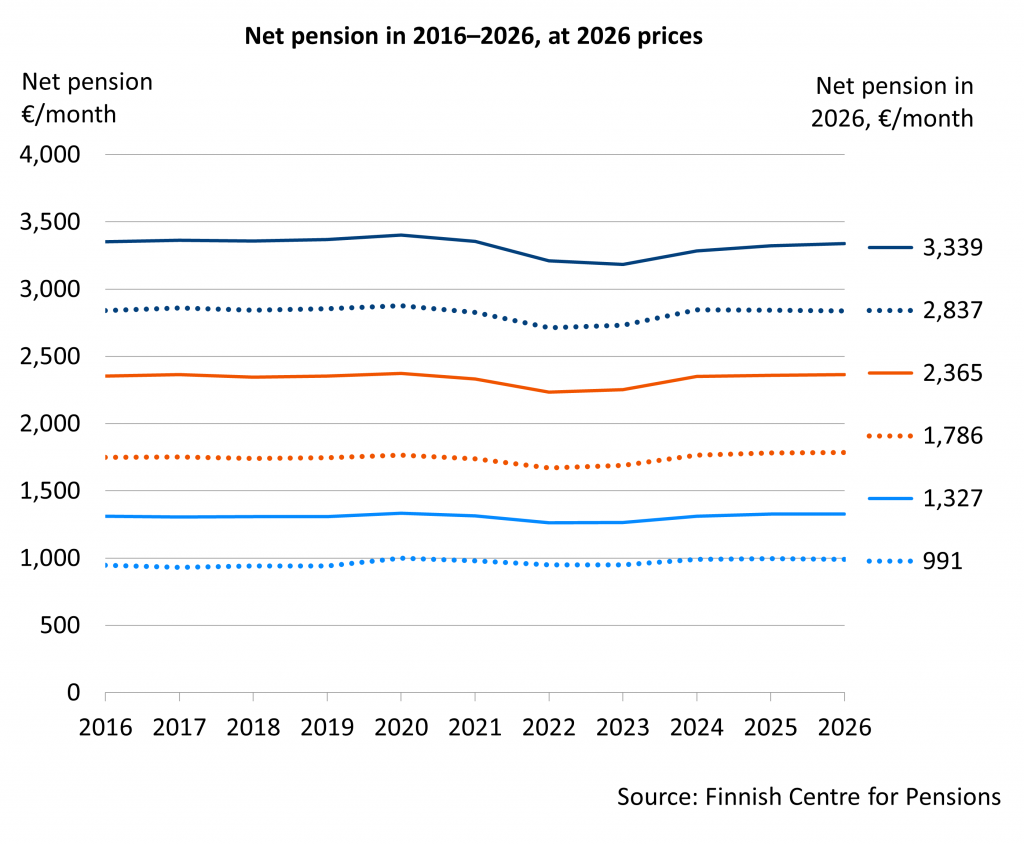

The graph below illustrates how pensions that started in 2016 have changed over the past decade. The euro amounts shown have been adjusted for consumer price changes to reflect the projected level for 2026, meaning the graph demonstrates how the purchasing power of pensions has evolved over the last ten years. Inflation for 2026 is assumed to be 1.1 per cent (Finnish Centre for Pensions’ economic forecast, 16 January 2026).

Over the decade, the pension of a pensioner receiving a pension from Kela only has increased in real terms by just under 5 per cent. Larger pensions have grown in real terms by up to around two per cent. At the highest income levels shown in the graph, pensions have decreased in real terms by less than one per cent.

Both pension and wage

Pensioners’ wage income is taxed on the same basis as any other wage income. The tax and contribution rate for a combination of pension and wage income is generally lower than for the same amount of income consisting of only a pension or a wage.

There are no restrictions on working while drawing an old-age pension; for pensioners on a disability pension, working is restricted by certain earnings limits. It is also possible for a person to receive pension income and wage income simultaneously if they continue working while withdrawing a partial old-age pension. The progressive tax scale eases the decline in total income if the income from work is reduced. Correspondingly, taxes will rise if a partial old-age pension is taken early on top of existing earnings.

The tables below show the tax and contribution rates calculated for various combinations of pensions and wages.

Table shows the tax and contribution rates for pensioners who in addition have a wage income. It also shows how large a share of the income from employment is lost to taxes and contributions.

For example, the tax rate for a monthly pension of 1,500 euros is 9.2 per cent. If the pensioner additionally earns 6,000 euros a year in wages, the tax and contribution rate for this additional income is 21.3 per cent. The tax and contribution rate for total income is 12.2 per cent.

The taxes and contributions are calculated for a 65-year-old pension recipient.

In the table the accrued amount of monthly pension is 1,500, 2,000 or 3,000 euros, and early payment of the pension is taken at a 50 per cent rate. The earliest full retirement age for the 1964 birth cohort is 65 years, and the pension is taken out 36 months early, bringing the total reduction for early retirement to 14.4 per cent. The partial old-age pension is also multiplied by the life expectancy coefficient confirmed for the first year of the pension.

The table describes different scenarios in which the individual does not work while on a partial old-age pension; does 50 per cent reduced working hours; or continues to work at the same wage level as before. As the partial old-age pension in the example starts at age 62, the individual will pay taxes and contributions applicable to persons under 65.